The Great Filter of Markets and Financial Intelligence

Building The Infrastructure of Reasoning for the Third Era of Investing

The financial markets operate as a continuous, ruthless evolutionary filter. They function as complex adaptive systems that actively select against irrelevance. Survival in this environment is an unending engineering challenge. Those relying on static tools to navigate a dynamic reality are winnowed out with unemotional efficiency.

We stand at the precipice of a third era in the history of investing. To understand its trajectory, we must understand the conflict that defines the current landscape. A great divergence exists. This divergence has created two distinct tribes that operate with fundamentally different assumptions about how the world works.

Two tribes. Both incomplete.

There exists a great divide in the world of capital allocation. It is a tribal war between the technologists of Silicon Valley and the veterans of Wall Street.

On one side you have the AI optimists. Led by VC and the AI talents, they are fluent in the languages of models and compute. They view the next improvement in investing as primarily an engineering challenge. They treat the markets as if they can be solved by prediction or dominated by the obvious winners of the artificial intelligence revolution. Their shorthand becomes a single bet on the hardware providers like Nvidia or the key stakeholders of the AI value chain. They believe that an AI native firm will inevitably replace the asset managers and the hedge fund in the near future through sheer processing power. They are wrong under real constraints.

On the other are market veterans. These are the survivors. They have lived through the cycles. They have seen bubbles inflate and burst. They respect price action above all else. For the discretionary managers, the rise of artificial intelligence is just another conventional productivity story to be absorbed gradually or a speculative excess that must revert to familiar valuation anchors. They rely on intuition, relationships, un-quantifiable deep domain knwoledge of the industry and the business models. They are skeptical of any technology that claims to supersede human judgment and agency. They are wrong as the regime shifts.

Each group is responding rationally to what it knows. Each group is incomplete.

However, within the intersection of the market veterans and the AI optimists, there exists a subgroup of systematic managers. They embrace the tools of large language models yet they understand deeply the limitations of inference speed and the nature of statistical hallucinations. They rejected deep learning models when others believed those models would create perfect prediction. They expand the dataset and take careful engineering of the data features. They examine the hypothesis with rigor. They priortize parsimony; and use the most explainable and reliable models that seems outdated to the AI natives. They prioritize robust logic over black box complexity. They know the market is an adversary.

Their methodologies and beliefs are what grounds us, but will not constrain us.

The nature of investors’ confusion

Markets rarely fail because people lack information. They fail because people misunderstand the system they are operating in.

We have never had more data, more commentary, more charts, more models, more conviction. And yet the gap between what people say they understand and what they actually trade has widened. This disconnect reflects a system whose underlying geometry has quietly shifted.

Periods of stability reward simple thesis. They allow familiar frameworks to work well enough, long enough, that confidence builds around them. Periods of transition punishes them. They expose the limits of those frameworks, often abruptly.

We believe the market is entering such a transition.

Artificial intelligence arrived as an investment theme, while quietly reshaping the constraints that link technology, capital allocation, labor, and geopolitics.

AI is not the only structural shift. Market microstructure and political economy are changing at the same time. The explosive growth of ultra-short-dated options, especially 0DTE, compresses risk, positioning, and hedging into the intraday tape. This tightens the feedback loop between price action, dealer hedging, liquidity, and volatility. In positive-gamma regimes, moves can be damped and price can pin and chop; the tape becomes messier and more range-bound even as headline volatility looks suppressed. Until exposures flip and the same mechanics can accelerate the move.

At the same time, a world of higher inflation uncertainty and populist pressure reshapes the policy reaction function, the credibility of institutions, and the risk premia investors assumed were stable. Old macro playbooks fail as the constraints governing policy and distribution shift, even though macro forces themselves remain central.. The market is still learning how to price those interactions.

As a result, we now operate in an environment where narratives feel decisive, because they are everywhere and emotionally coherent, while structure is indecisive, because it is binding. Investors are surrounded by information, yet remain unprepared for how the system behaves under stress. They feel informed, but they are positioned using models built for a different regime.

Market Reasoner exists to address that gap.

Markets as systems, not opinions

We do not think markets can be understood as a collection of opinions waiting to be aggregated into a forecast. We think of them as systems that evolve under pressure.

Liquidity expands and contracts. Volatility clusters and breaks. Positioning builds until it cannot. Feedback loops form between price, behavior, and capital flows. None of this is new. What is new is the set of forces now shaping those dynamics. In the stochastic uncertainty of the random walk, there is mechanical certainty.

But market is a complex adaptive system. It is composed of millions of agents who are all learning. When a strategy becomes popular it changes the market dynamics. The organism adapts. The strategies that worked ten years ago may not work today. Alpha decays. The new sources of alpha are found in the deep causal chains that link a supply shock in one part of the world to a price movement in another. To navigate this system we must be hyperrealists.

In such systems, prediction rarely survives regime change. Reasoning endures longer.

Reasoning means asking what constrains behavior, not what confirms beliefs. It means paying attention to second-order effects, not just first-order narratives. It means staying humble about what cannot be known, while being disciplined about what can be observed.

This perspective informs everything we write.

A grounded view of artificial intelligence

We treat AI as a production system with physical limits and empirical constraints.

A serious view of AI follows the entire chain. It begins with research and training dynamics, extends through data curation and reinforcement learning, and ends in physical infrastructure. Compute is not an idea. It is capital expenditure, power availability, cooling capacity, and geopolitical supply chains. GPUs are constrained resources subject to industrial and political realities.

Scaling introduces bottlenecks, trade-offs, and nonlinear effects that are often ignored in surface-level commentary. Over time, data quality becomes as binding as data quantity. Alignment and post-training shape behavior as much as raw capability. These dynamics matter economically, not just technically.

Markets are not pricing AI in isolation. They are pricing how AI interacts with interest rates, margins, labor substitution, capital cycles, and national strategy. Most analysis stops before these interactions become uncomfortable.

We do not.

The Illusion of the AI Trader

The integration of artificial intelligence into investing is currently dominated by a dangerous illusion that ignores the fundamental mechanics of the technology. We see a prevalent belief in the autonomous agent that can read news, analyze financial statements, and execute trades in a seamless loop.

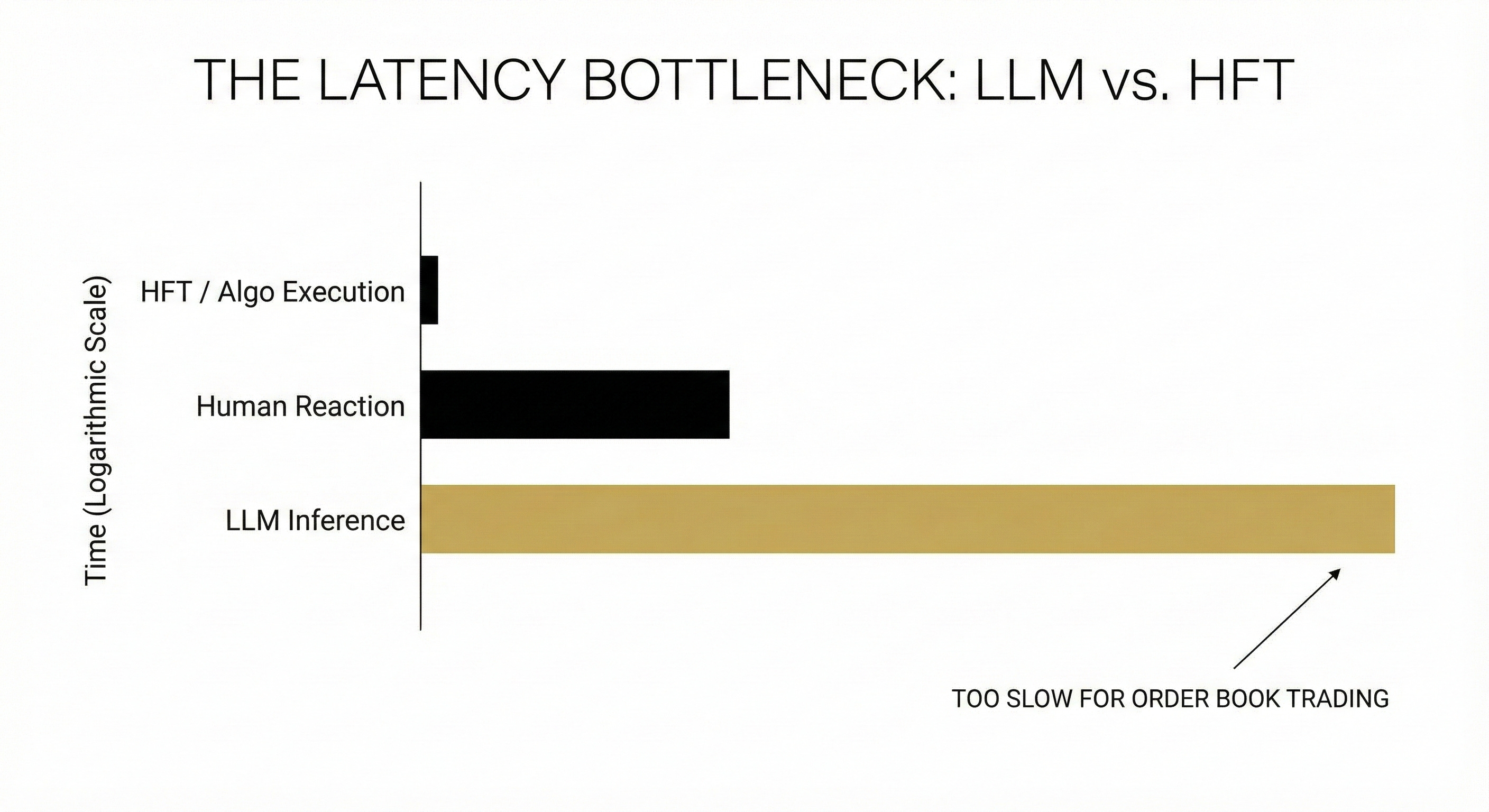

We must look at the mechanics of how these models actually think. Unlike traditional algorithms that react in microseconds, large language models must generate output sequentially. This process is bound by memory bandwidth rather than processing power. Moving the weights of a massive model from memory to the processor takes tens of milliseconds. In modern markets this is an eternity. By the time an agent processes the order book the price has likely moved. The agent ends up trading on stale data and suffers from immediate adverse selection. In the domain of speed you are either the fastest or you are extinct.

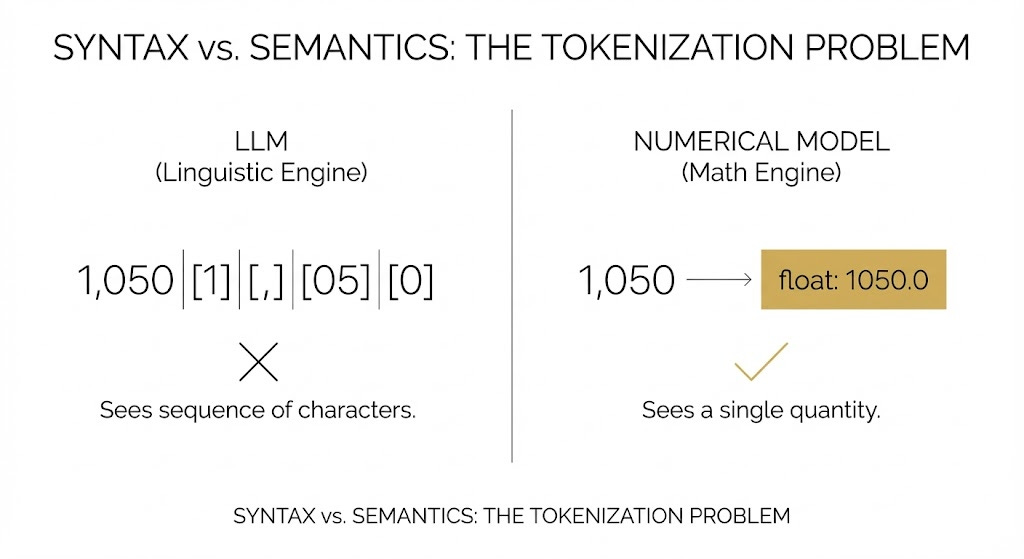

The deeper problem lies in the nature of the intelligence itself. The fundamental limitation of the Large Language Model is that it is a heavily parameterized autoregressive transformer. Its core objective function is not truth or value, but the minimization of perplexity in predicting the next token. These models are linguistic engines rather than numerical ones; and they are certainly not causal reasoners. When asked to optimize a portfolio or calculate risk, a model often produces a hallucination that looks plausible but is factually incorrect. It mimics the syntax of logic without understanding the rules of arithmetic. Relying on a probabilistic language model for precise capital allocation introduces a layer of fragility that is unacceptable in a high-stake financial system. It creates a black box that cannot be audited.

Most general purpose models fail in adversarial environments because they lack regime recognition. They are conditioned on historical distributions, and inevitably break when the correlations that defined the past decouple in the present. We see this limitation as a structural barrier to autonomy.

We will expand on the architectural solutions to these problems and the concept of neurosymbolic engineering for alpha research in a subsequent report.

Quantitative investing without mythology

Quantitative investing is often misunderstood in two opposite ways.

On one hand there is the superstition of the black box where observers believe that sufficient compute and feature engineering will inevitably yield a crystal ball that forecasts returns.. On the other hand, there is the cynicism that views the entire discipline as an exercise in data mining. In which relationships are spurious and performance is merely a lucky streak waiting to revert. Both views are convenient. Both are wrong.

Systematic investing is the industrialization of the scientific method applied to financial time series. It is a discipline of measurement, inference, and risk-taking under uncertainty. It spans the entire spectrum of market mechanics and time horizon, from the mean reversion of statistical arbitrage and the structural harvest of carry to the convexity of trend following. The discovery of a signal is only the beginning of the problem.

It demands respect for the friction of the market as much as the purity of the mathematical model. We place equal weight across data engineering, inference, portfolio construction and monetization because the theoretical alpha of a model is meaningless if it is destroyed by the reality of execution and liquidity and market impact. We utilize econometrics and causal inference as powerful tools to separate signal from noise. But we do so with humility. Identification fails when regimes shift and correlations break.

In a system defined by entropy and competition, what survives is not complexity, but robustness.

Experience, not doctrine

Our thinking is shaped by multiple traditions. You will see the influence of Druckenmiller in the attention to regime shifts, of Eugene Fama in the emphasis of empirical over theoretical, of Pring in the respect for structure, of Soros in the recognition of reflexivity, and of Tudor Jones in the primacy of risk control. These are not styles to imitate, but methodology to internalize.

Behind this writing, is a team of AI researchers, quants, traders, and seasoned portfolio managers. We respect and understand the boundaries of our respective domain expertise. We empower one another while grounding the collective intellect in the harsh constraints of reality. We believe only in the significance of empirical evidence. We respect the feedback of the market above the elegance of any theory.

We do not believe in fixed playbooks. We believe in adapting frameworks. That requires patience, and it requires accepting that clarity often comes later than discomfort.

What this publication is for

Some readers will come looking for answers. Others will arrive looking for a way to think more clearly about uncertainty.

We do not discourage the first impulse, but we write for the second.

We will not present forecasts as truth or treat short-term accuracy as virtue. What we aim to offer is something less immediate and more durable: a way of reasoning alongside us as markets evolve, constraints shift, and regimes reveal themselves. We offer a peek into the engineering of how we build the infrastructure of market reasoning.

If this sounds unsatisfying, that is understandable. The market often rewards decisiveness in appearance. Over time, it rewards discipline in reality.

A final note

This is not an investment newsletter in the conventional sense. It is a research-driven publication about how to think about the market when familiar frameworks stop working as expected.

It will attract disagreement. That is healthy. It will attract attempts at imitation. That is inevitable.

Our responsibility is to remain honest about what we know, precise about what we do not, and rigorous about the difference.

Markets, without illusion.

AI, without hype.

Disclaimer

This newsletter and any related emails (the “Publication”) are provided for informational and educational purposes only. They do not constitute an offer, solicitation, or recommendation to buy, sell, or hold any security or other financial instrument, nor should they be interpreted as legal, tax, accounting, or investment advice.

The Publication is general in nature and has been prepared without regard to the investment objectives, financial situation, or particular needs of any specific person. You should conduct your own independent research and consult with a qualified financial adviser before making any investment decision. The information contained in the Publication is based on sources believed to be reliable, but its accuracy, completeness, or timeliness cannot be guaranteed. All information and opinions are subject to change without notice.

Investing involves significant risks, including the possible loss of principal. Past performance is not indicative of, and does not guarantee, future results. The views expressed in the Publication are those of the authors and Market Reasoner. The authors and related parties may hold or acquire positions in securities, instruments, or issuers discussed and may buy or sell such positions at any time without notice.

Neither the author(s) nor any publisher, affiliate, director, officer, employee, or agent accepts any liability for any direct, indirect, incidental, consequential, or punitive damages arising out of the use of, or reliance on, the Publication.